Are you only making minimum payments on your credit cards?

If you're only making the minimum monthly payment on your credit cards, you could be paying off that debt for decades! A 'minimum monthly payment' is the lowest amount you can pay toward your monthly credit card bill in order to keep the account current. However, too many of us make JUST the minimum monthly payment. Allow us to explain why that's not the best way to pay down your credit card balances and how that practice can keep you in debt for a lot longer than you think.

Credit Card Interest Rates: Think Before You Swipe!

Credit cards are a powerful spending tool, but they can also be a detriment to our financial condition if not used properly. Many times when someone is choosing whether or not to purchase an item with their credit card, they decide whether or not it fits into their monthly budget by determining the amount of the minimum monthly payment for that purchase. Unfortunately, people often fail to understand the principles of how credit card interest is calculated, and how much of their minimum payment actually goes towards paying down the debt. We'll provide you with some basic information about how credit card companies calculate the amount of your minimum monthly payment and why it's important to always pay a bit more.

Credit card interest rates vary depending on your credit profile. Someone with a 750 FICO score may be paying a 4% Annual Percentage Rate (APR), while someone with a 620 score may be paying 14% (or much higher) for the same purchases. Your APR is the amount of interest that you will annually pay on your balance. If you pay off your balances in full each month the APR doesn't make all that much of a difference. Yet for many of us, paying the balances in full every month just isn't possible. That's fine too, but you should plan to pay the balances as soon as you are able. The faster you pay off your balances, the less money you'll spend on interest, or you could think of it as the sooner you pay off your credit card debts, the more money you'll save in the long run. In this economy, money is tight and unexpected expenses can make it impossible to pay anything more than the monthly minimum payment, but you should never construct your credit card spending decisions on what you think your minimum payment will be. Your interest rates are going to be the most important reason for striving to pay more than the minimum each month. Interest rates can make your purchases MUCH more expensive than you bargained for. How your interest is calculated might not be what you expect.

How Credit Card Interest Rates are Calculated

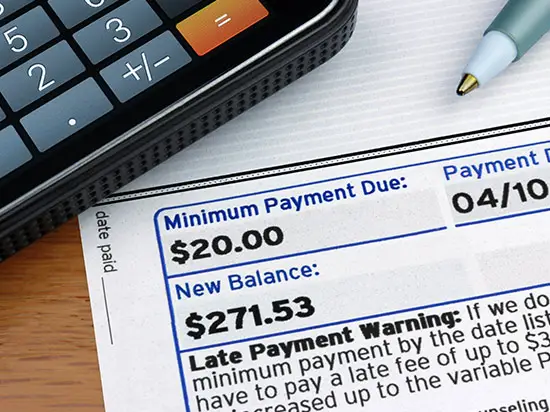

Let's say that you buy a new TV for $1,000 with your credit card that has an APR of 18%. You get the bill next month and all they are asking for is a minimum payment of $20. No big deal, right? First you think, "No problem, I can easily afford $20 per month!" Then you do some quick math in your head: "At $20 per month, I'll have this TV paid off in about 4 years, then I'll be ready to upgrade." Right? Wrong!

The problem with the "quick math" used in this example is that it fails to include the fact that interest on a credit card is "compounded", meaning that the interest is added to your total balance. If your balance isn't paid off at the end of each month, you'll be paying interest on top of that interest because it's now a part of your balance. Since credit cards are revolving lines of credit, the issuers will typically calculate the interest on a monthly basis. This can be calculated simply by taking your APR and dividing it by 12 (months). So, if your APR is 18%, your monthly interest rate will be 1.5%:

Monthly Interest Rate % = Annual Percentage Rate / 12 (months)

Calculating Your Credit Card Minimum Monthly Payment

Usually, your minimum monthly payment is 2-4% of the principal balance depending on your banking institution. Let's say that your monthly payment will be 2% of the principal balance. That means, on a $1,000 purchase the minimum monthly payment you will be asked to make is $20 ($1,000 x 2% = $20). How much of that payment will go toward paying the principle balance?

Well, we've already figured out that the monthly interest rate (based on an 18% APR) is 1.5%. So, your credit card company will be charging you 1.5% interest on your balance every month. We can now take the balance of $1,000 and multiply it by the 1.5% which gives us a monthly interest payment of $15. Now you're seeing the problem, right? You've just made a minimum payment of $20 toward your $1,000 TV purchase and $15 of that payment will be used to pay just the interest. This leaves only $5 of your $20 minimum monthly payment actually going towards paying down your debt!

How Long Will It Take to Pay This Credit Card Balance Off?

If you were to make no other purchases using this particular credit card, and you paid just the minimum payment every month, it would take you about 151 months to pay off this TV. That's a little over 12 years! Think that's scary? How about this: based on our example of an 18% APR, you will pay $1,396 in interest over the course of those 151 months.

So, the $1,000 TV that you just had to have, but could only afford by putting it on a credit card has now cost you a total of $2,396 and has taken you 12 years to pay off.

This is why it's so important to make more than the minimum payments on your credit cards whenever possible. Using our same $1,000 purchase at an 18% APR, if you were to pay $100 per month toward this purchase, it would only take you 11 months to pay the balance in full and you'd only have paid $91.62 in interest charges. This may seem a bit more expensive than you intended, but wouldn't you agree it would be worth it in the end?

To avoid carrying debt with you for years, or even decades, you must think of these types of scenarios before using your credit cards to make purchases. Using this methodology, you should be able to get a good idea of what your minimum monthly payment AND your interest charges will be before you charge something. You should also be able to figure out how much you'll have to pay each month in order to get the balance paid in full in 4-6 months, which is what we recommend. If you need help figuring out your credit card repayment options, there are plenty of online calculators and smartphone apps that do the math for you.

Perhaps the most important thing to think about is whether or not you can realistically afford the added expense. The easiest way to determine this is to look at your household budget. Do you have expendable income? Can you safely take on another monthly expense and still meet your other obligations? If you're not sure, or if you don't have a budget yet, it's time to sit down and create one. A budget keeps your finances in check and leaves little room for surprises. A current budget is advantageous for any household income because the easiest way to let your finances get out of hand is to pay as little attention to them as possible.

All of the figures used in this article such as your APR, the percentage of your balance used as a minimum payment, etc., will be different for every credit card issuer. So, it's important that you understand the terms of your credit card. These terms will be clearly outlined when you sign up for a new credit card. Pay close attention to all of the terms and make sure that you understand what they mean. Hopefully, you're armed with knowledge about minimum monthly payments and interest rates now.

We do not want to dissuade you from using credit cards. Again, they can be a very helpful spending tool if used properly and responsibly, and they certainly come in handy when you encounter emergency expenses that you did not budget for. However if you're not careful, the decisions you make at the checkout counter can have lasting consequences for years and years to come. H. W. Shaw may have said it best: "Debt is like any other trap...easy enough to get into, but hard to get out of."